Research question and hypothesis

A rough backbone should explain structural medium/long dynamics, but not necessarily event-rich short expiries.

The source is the first complete, non-partial `svi_surface_snapshot` received at 2026-07-08 07:59:28.360 UTC. The hypothesis was deliberately split: rough dynamics may be useful at 30 days and beyond, while a separate premium layer may be necessary below 30 days.

No raw exchange books or historical sample are claimed. This is a single-snapshot model comparison, not evidence of live strategy performance.

Implementation

The comparison fixes the data grid, seed and Monte Carlo design.

- 12 SVI expiry rows reconstructed on 11 log-moneyness points from -0.55 to 0.55.

- Five expiries at or beyond 30 days used for backbone calibration.

- 16,384 common-random-number paths for the backbone and 32,768 for short-tenor diagnostics.

- Random seed 7,071,726 with antithetic variates.

- Scipy robust least squares with soft-L1 loss and recorded standard/widened bounds.

- Calendar total variance, butterfly-convexity proxy and call-monotonicity grid checks.

The exact bounds, discretisation, interpolation and source-artifact hashes are in the machine-readable manifest.

Candidate comparison

Fit quality and scenario suitability lead to different selections.

| Candidate | Scope | RMSE | Decision |

|---|---|---|---|

| Global rough-vol backbone | >=30d | 1.25 | Useful baseline; H and eta press against bounds. |

| Term-structured backbone | >=30d | 0.86 | Selected medium/long scenario backbone. |

| Term backbone implied short | <30d | 27.88 | Rejected: short-tenor implication is unusable. |

| Term backbone + raw short overlay | Full | 0.58 | Best in-sample fit benchmark; not used for shocks. |

| Term backbone + smooth premium | Full | 7.08 | Selected smooth parameter-shock base. |

Failure case

Wider parameter bounds do not repair the short-tenor model class.

Widening H, eta, rho and forward-variance scale bounds improves medium/long RMSE by only 0.02 vol points while pushing eta to the new cap. Independent short fits also remain unstable near expiry. The evidence points to event, jump, flow or microstructure premium rather than a simple optimiser-bound problem.

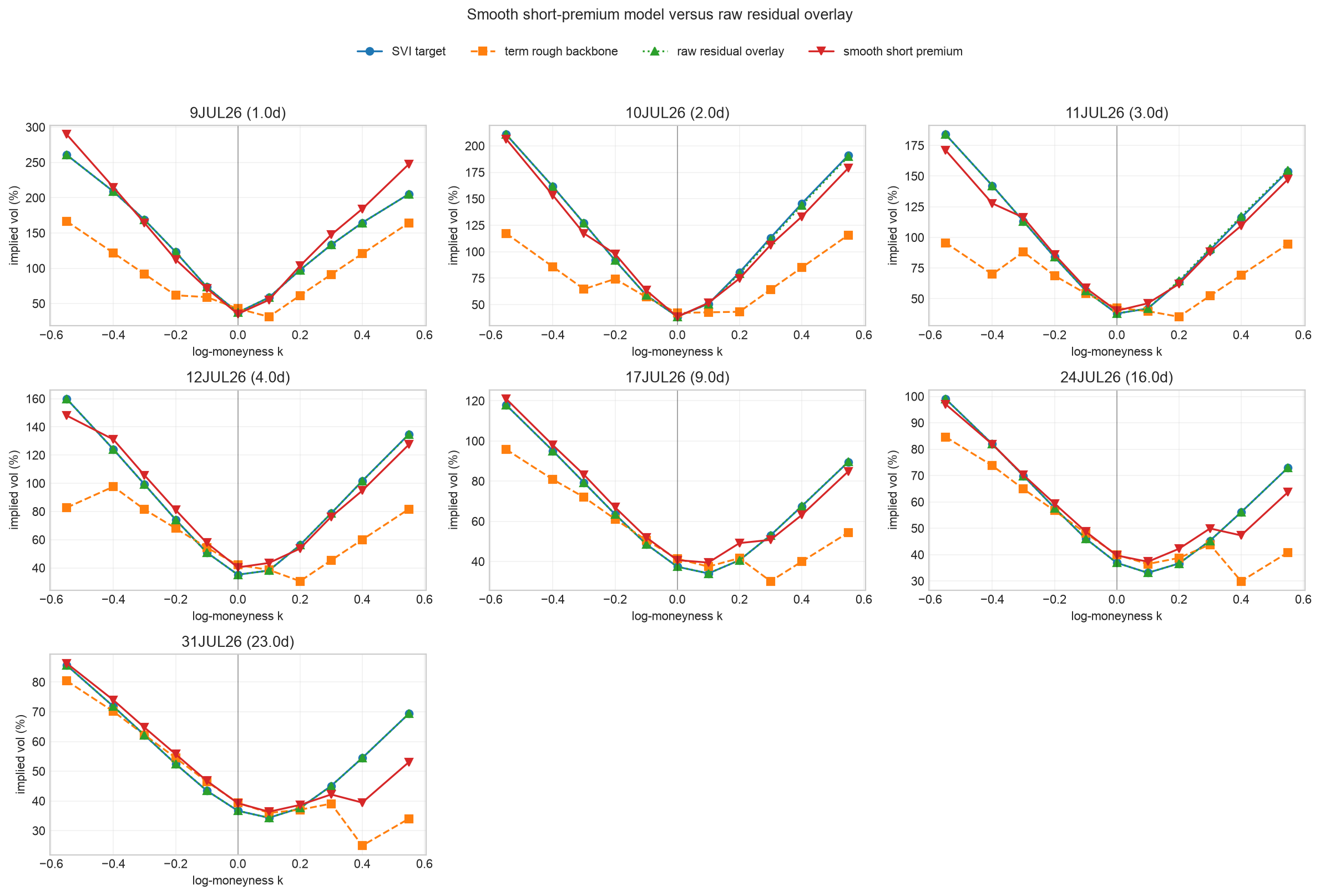

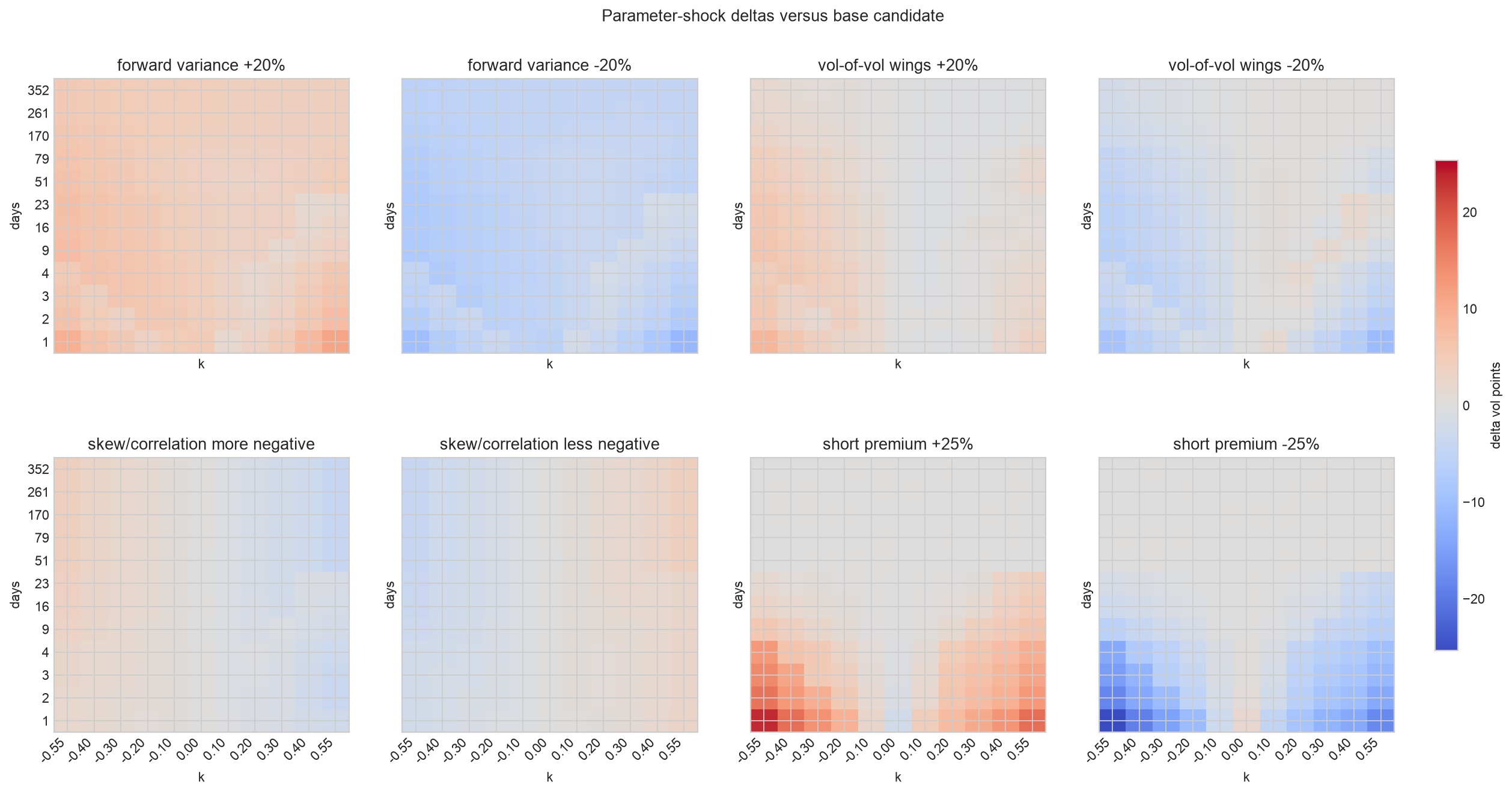

Scenario selection

The raw overlay is a fit benchmark; the smooth premium is the shock base.

A raw residual overlay reaches 0.58 vol-point full-surface RMSE, but shocking raw IV residual points produces lumpy surfaces. The parameter-based scenario base therefore uses the term-structured backbone plus a smooth total-variance short-premium layer, accepting higher in-sample error for cleaner, inspectable shocks.

Reproducibility

The result package identifies the source, code revision and environment.

Known limitations

This is a research prototype, not production calibration evidence.

- Only one frozen surface is evaluated; multi-snapshot stability is unknown.

- The short-tenor implication fails and requires a separately labelled premium layer.

- The best raw-overlay fit is in-sample and unsuitable for direct shocks.

- Grid diagnostics are not a complete production static-arbitrage proof.

- Raw market data is not redistributed, limiting exact independent reconstruction of the source snapshot.