The core idea

Rough volatility models volatility as irregular at every horizon.

In a smooth stochastic-volatility model, variance evolves like a relatively regular diffusion. Rough volatility changes that assumption: the variance path is much less smooth, which helps the model reproduce the way option markets price fast volatility movement and persistent smile dynamics.

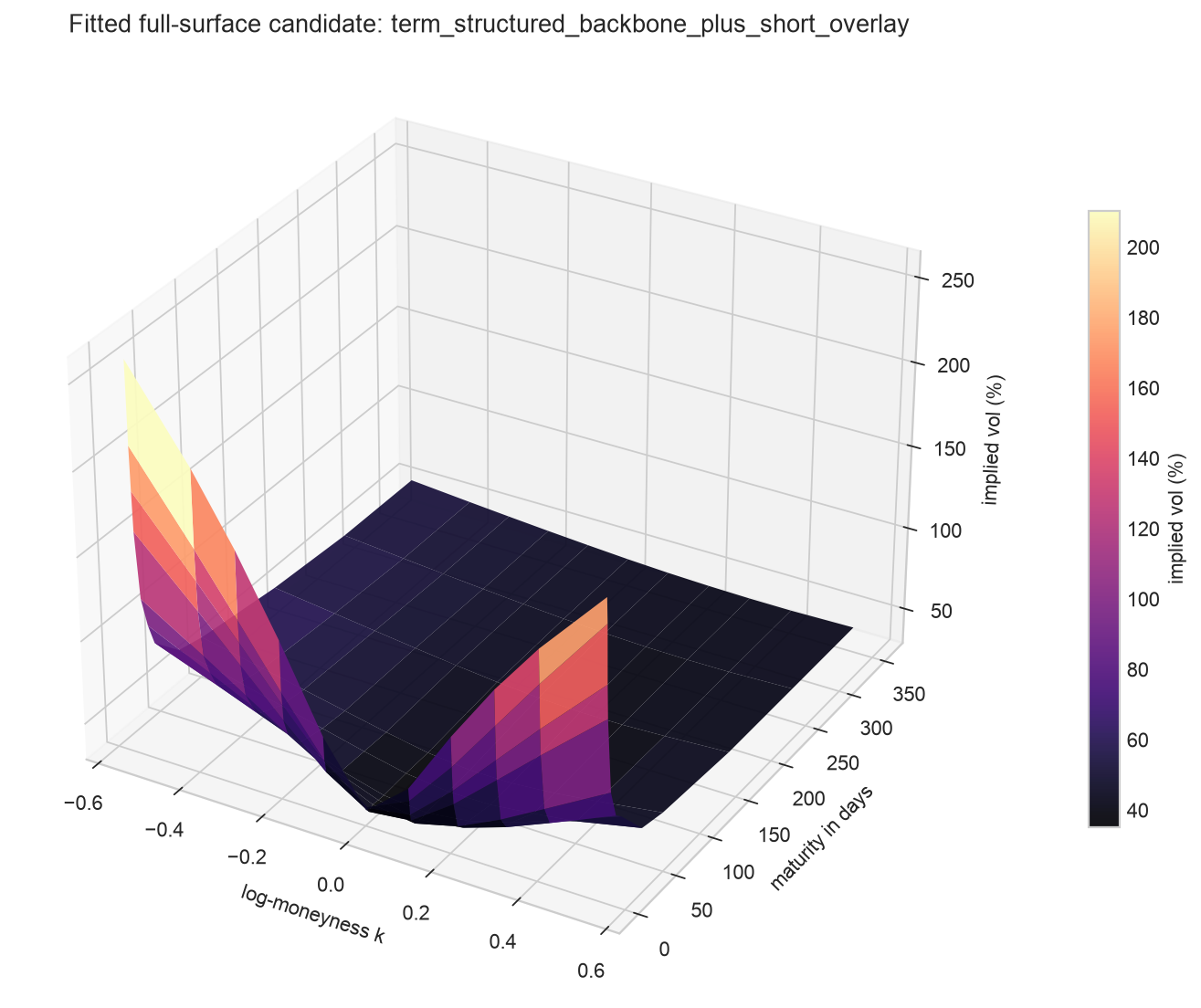

For a crypto options volatility surface, rough volatility is most useful as a scenario backbone. It gives the surface a dynamic rule for how ATM volatility, skew, wings, and term structure should respond when spot and forward variance move.

Term-structured rough-vol backbone

The medium and long expiries use a rough Bergomi-style backbone with maturity-varying vol-of-vol and skew/correlation. It gives the scenario engine structural dynamics instead of only interpolating SVI slices.

Short-tenor premium layer

The shortest crypto expiries contain event, flow, and microstructure premium that a continuous rough diffusion does not imply from the longer tenors. That premium is modelled separately.

Parameter-based shock surface

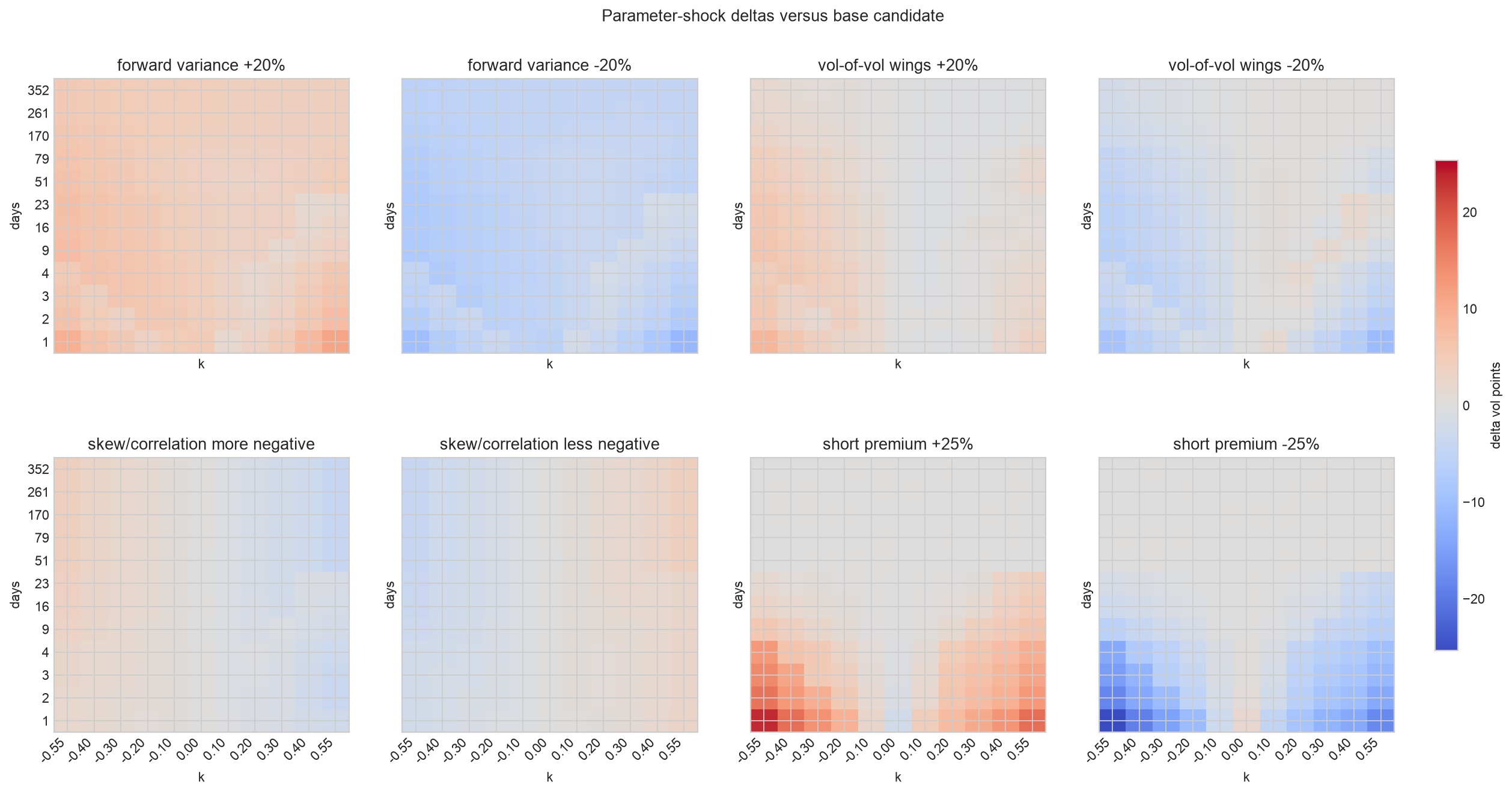

For scenarios, Derivasys shocks forward variance, wing intensity, skew/correlation, and short-premium strength. A smooth total-variance premium layer is used so shocks do not inherit raw residual lumps.

The current Derivasys research conclusion is deliberately not "pure rough Bergomi fits everything." The useful stack is a rough-vol medium/long backbone plus a separately controlled short-tenor premium layer.

Rough Bergomi intuition

Rough Bergomi turns forward variance, vol-of-vol, and skew into a dynamic smile model.

Rough Bergomi is a practical benchmark for rough volatility. It starts from an initial forward variance curve, then evolves the variance process with roughness, vol-of-vol, and spot/variance correlation. In options language, those parameters shape the level, skew, wings, and scenario response of the implied volatility surface.

rough_vol_surface = price_options(S0, xi(t), H, eta, rho, expiry, strike)Hurst exponent H

Controls how rough the volatility path is. A small H means volatility can move in a jagged, persistent way that better resembles option-market volatility dynamics than a smooth diffusion.

Vol-of-vol eta

Controls how strongly the variance process moves. In the Derivasys snapshot, a simple global fit pushed eta to its bound, which is diagnostic rather than a reason to keep widening bounds.

Skew/correlation rho

Links spot moves and variance moves. Negative rho creates leverage-style behaviour: spot down tends to lift implied volatility and steepen downside skew.

Forward variance xi(t)

Provides the initial term structure. The model is calibrated in total-variance space so expiry smiles, forwards, and scenario tenors remain comparable.

Derivasys modelling stack

The practical model separates structural rough-vol dynamics from short-tenor premium.

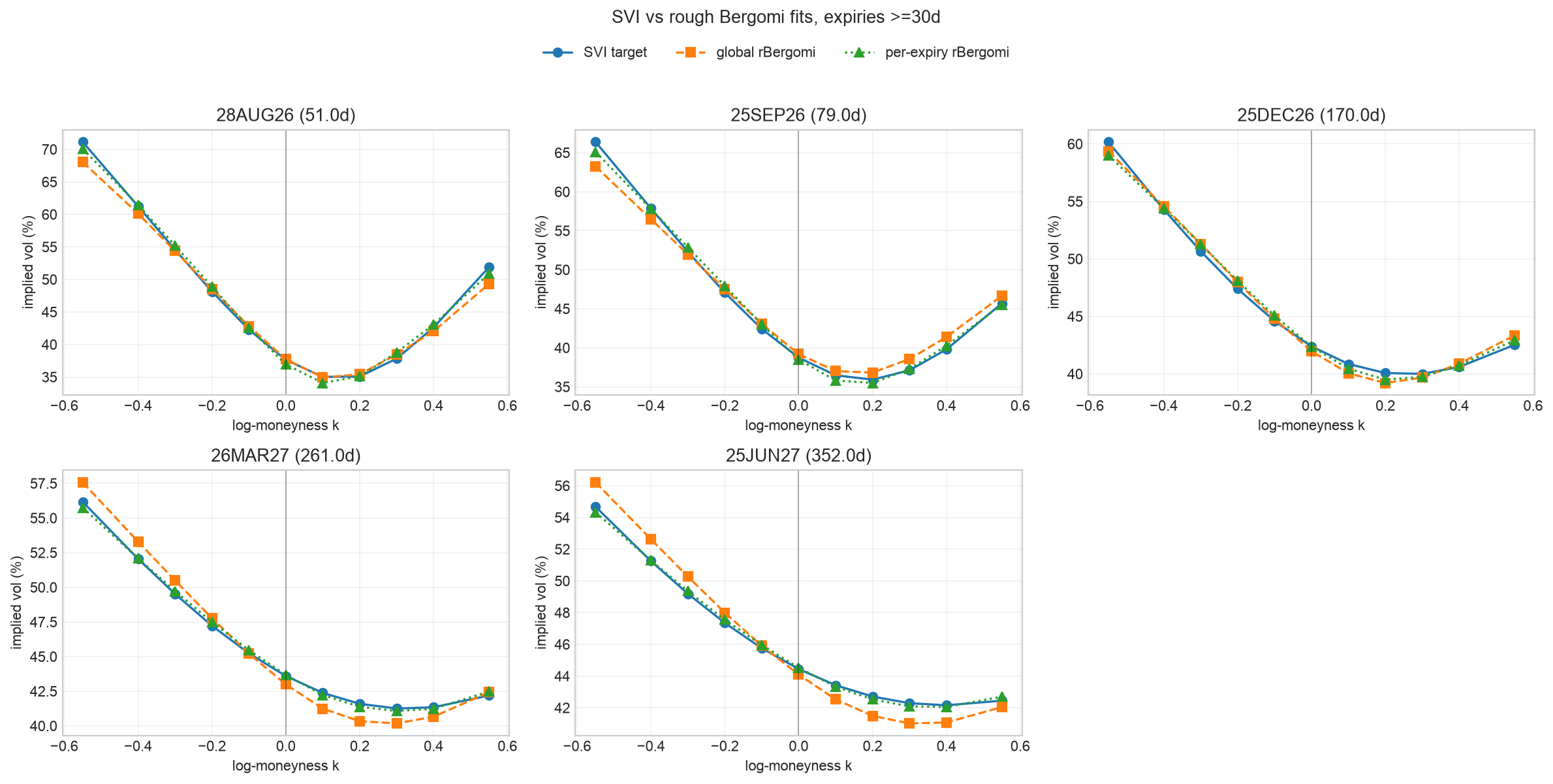

The research notebook freezes one Derivasys SVI snapshot, reconstructs the SVI surface from the published parameters, and calibrates rough-vol candidates against that surface. The best practical stack uses term-structured rough-vol dynamics for expiries of 30 days and longer, then adds a dedicated short premium layer for the front of the surface.

term-structured rough-vol backbone for >=30d + raw short residual overlay as the fit benchmark + smooth total-variance short premium as the shock base

This distinction matters. The raw overlay tells us how close the current snapshot can be matched. The smooth premium layer tells us how to shock the short end without turning static residuals into unstable surface artefacts.

Calibration evidence

The medium/long backbone is useful; the pure short implication is not.

On the July 8, 2026 Derivasys SVI snapshot, the medium/long rough-vol fit is strong enough for scenario research. The same fit does not imply the short end. That failure is the main reason the model needs a short-premium layer rather than more aggressive global parameter bounds.

| Candidate | Scope | RMSE | MAE | Max abs | Read |

|---|---|---|---|---|---|

| Long-fit rough Bergomi backbone | >=30d | 1.25 vol pts | 0.95 vol pts | 3.97 vol pts | Good medium/long structural backbone. |

| Widened-bound backbone | >=30d | 1.23 vol pts | 0.93 vol pts | 3.83 vol pts | Only 0.02 vol points better, while parameters become more extreme. |

| Term-structured eta/rho backbone | >=30d | 0.86 vol pts | 0.59 vol pts | 3.73 vol pts | Best current medium/long backbone without relying on raw short residuals. |

| Long-fit rough-vol implied short | <30d | 28.17 vol pts | 15.66 vol pts | 112.04 vol pts | Long-end rough-vol fit does not imply short-tenor crypto wings. |

| Term backbone plus raw short overlay | Full surface | 0.58 vol pts | 0.27 vol pts | 3.74 vol pts | Best in-sample fit benchmark, but not the preferred direct shock surface. |

| Term backbone plus smooth short premium | Full surface | 7.08 vol pts | 3.66 vol pts | 38.49 vol pts | Cleaner parameter-shock base; gives up exact raw residual interpolation. |

Widening the global bounds lowered the 30-day-and-longer RMSE from 1.25 to 1.23 vol points, while pushing eta to the wider cap. That is a warning sign, not a production modelling win.

Why the short end is different

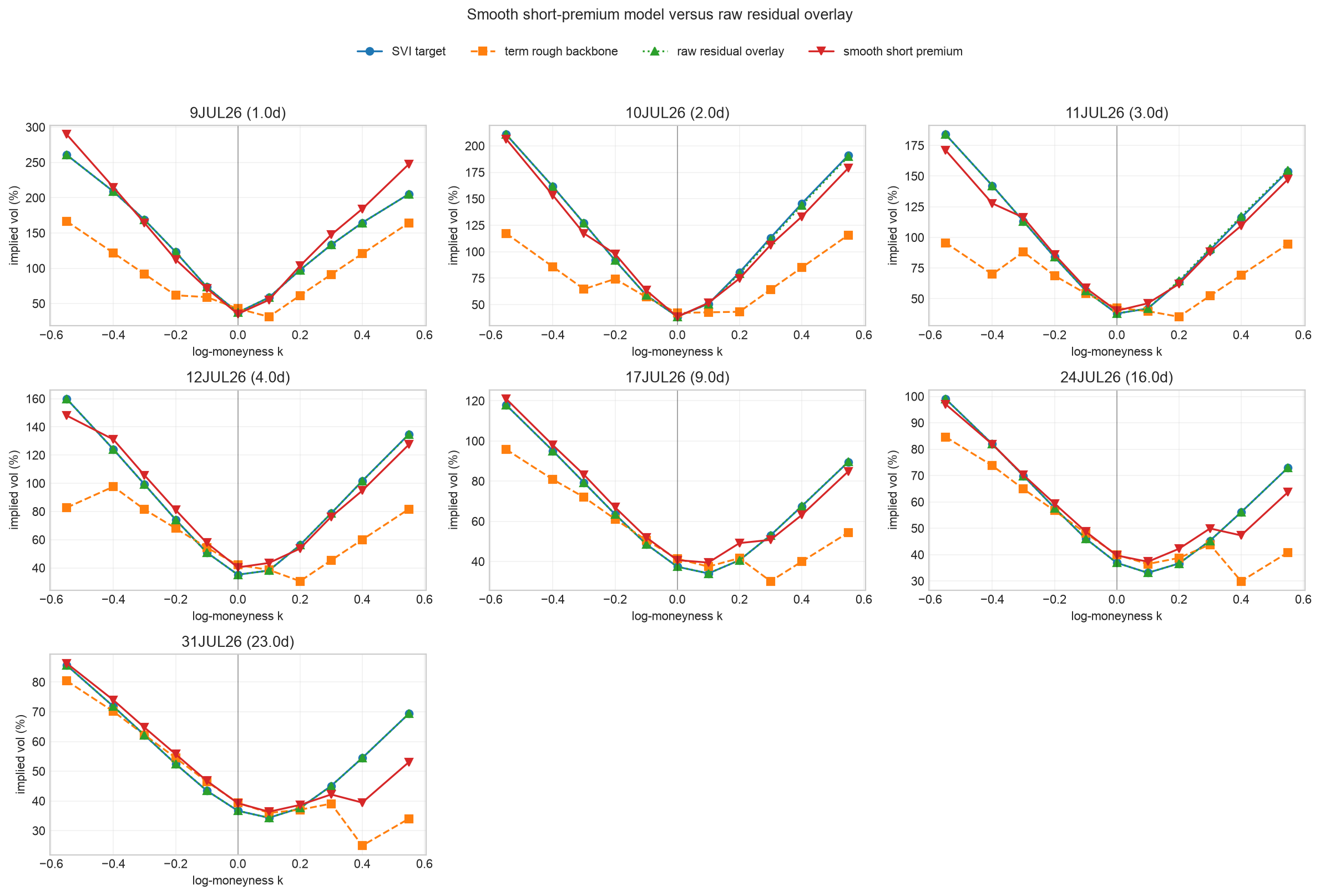

The shortest crypto expiries price event premium that the long-end rough-vol fit does not imply.

The short-end problem is not just a weak optimiser result. Pure rough-vol extrapolation, term-structured rough-vol, per-expiry short local rough-vol, and a simple two-sided jump/event layer all fail to match the front-expiry wings well enough. That points to a separate event/flow premium component.

Near-expiry wings are event heavy

Crypto short expiries can price exchange incidents, macro prints, ETF headlines, unlocks, liquidation cascades, and weekend gap risk. Those premiums are not simply the short-time limit of a medium/long rough diffusion.

Pure short local fits remain unstable

Independent rough Bergomi fits improve some 14-30 day expiries, but the sub-7 day bucket stays poor even with more paths, antithetic variates, and finer time steps.

Bounds are a symptom, not the fix

Wider bounds barely improve the medium/long fit and push parameters into more extreme values. That points to model-class mismatch in the short end, not just an optimizer range problem.

Raw overlays fit but shock badly

A raw residual grid can match the short SVI surface in-sample. If it is shocked directly, local residual bumps turn into visible lumps and jumps across moneyness.

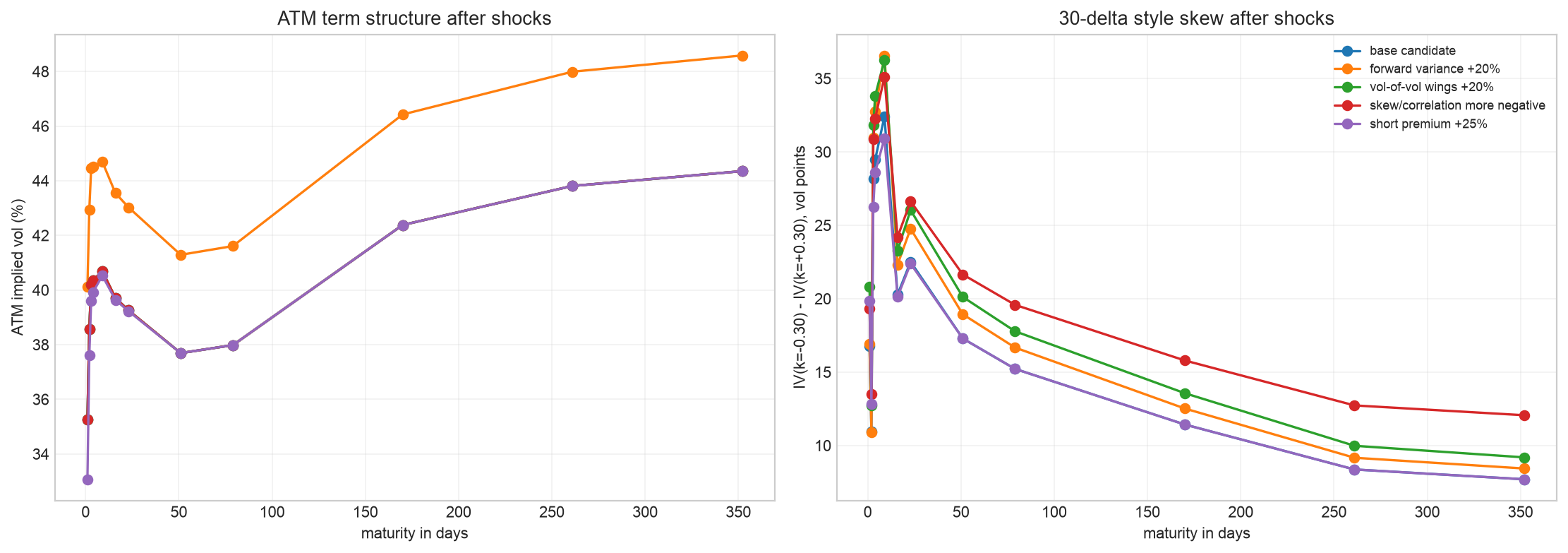

Scenario shocks

Shocks should move parameters and total variance, not raw IV residual points.

The weird lumps seen in rough-vol shock plots come from shocking a raw residual overlay. That overlay is allowed to fit the in-sample short SVI grid very closely, but it is not a stable dynamic object. For scenario work, a smoother total-variance short-premium layer is a better base.

Forward variance shock

Moves the base term structure while preserving the connection to total variance and calendar checks.

Backbone wing intensity

Changes the amount of rough-vol smile convexity and tail richness without editing one strike at a time.

Skew/correlation tilt

Changes the spot/vol leverage effect and downside versus upside wing response through model parameters.

Short-premium intensity

Scales the smooth event/flow premium layer so short expiries can be stressed without injecting raw residual-grid artefacts.

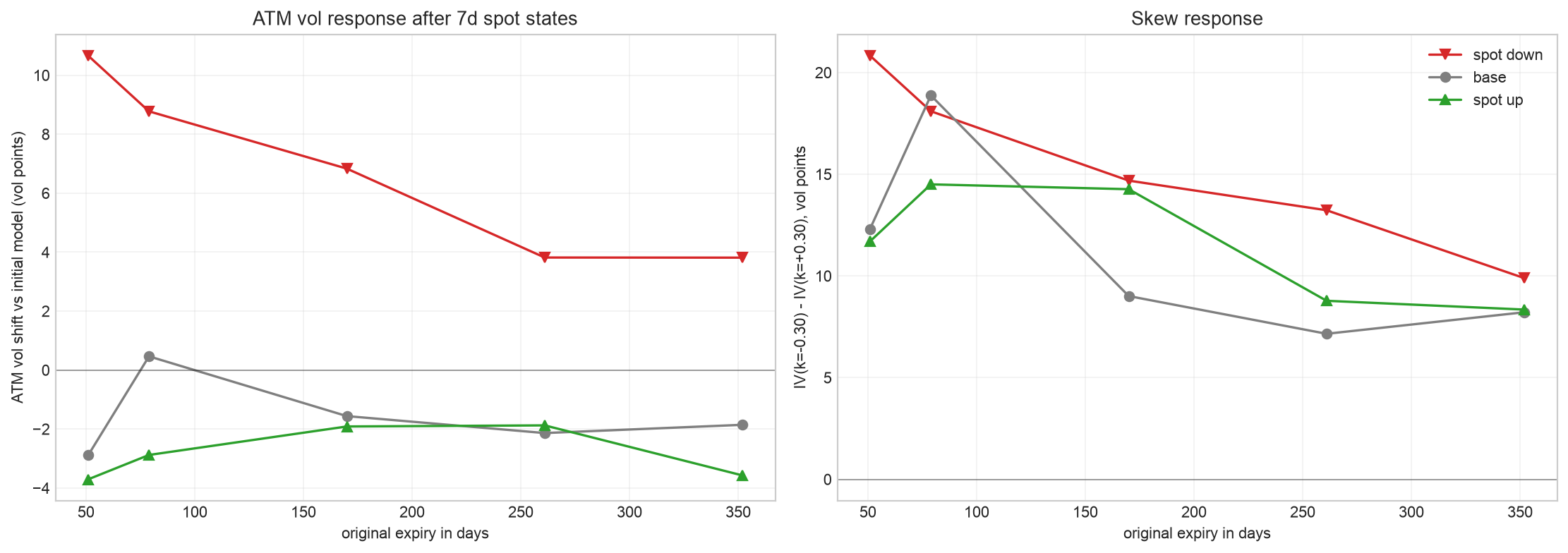

Spot and vol effects

Rough-vol scenarios can show spot-up, spot-down, and volatility-response states together.

In the current seven-day scenario experiment, spot-down paths average a -9.98% spot move and a +7.41 vol-point ATM response. Spot-up paths average a +9.41% spot move and a -3.11 vol-point ATM response. That is the kind of leverage effect a rough-vol backbone is useful for exposing.

-9.98% average spot move, +7.41 ATM vol points.

Surface remains close to the calibrated SVI snapshot.

+9.41% average spot move, -3.11 ATM vol points.

Use the same scenario state for skew, wings, Greeks, and term structure.

Production controls

A rough-vol scenario page still needs surface diagnostics and calibration governance.

The prototype is good enough to explain the rough-vol scenario design, but it should not be oversold as production calibration infrastructure. The next step is to repeat the analysis across snapshots, strengthen the arbitrage controls, and define the production API shape for scenario inputs and outputs.

Grid-level no-arbitrage diagnostics

The current prototype checks calendar total variance, a butterfly convexity proxy, and call monotonicity on the research grid. The latest base and shock grids have zero violations on those tests.

Continuous-domain controls

The grid checks are useful diagnostics, not a full proof. Production modelling should extend the repair and constraints beyond the sampled moneyness and tenor grid.

Multi-snapshot stability

The current evidence comes from a frozen Derivasys SVI snapshot. Production use needs repeated calibration across live snapshots to test parameter, overlay, and shock stability.

Scenario pricing controls

Conditional spot/vol scenarios are still Monte Carlo based and can be noisy in far wings. Production scenarios need stronger variance reduction or pricing controls before exposing exact numbers.

API shape

A scenario API should identify the source surface, model layer, and shock controls.

Downstream systems need to know whether a value is live market state, a raw fit benchmark, or a scenario output. The rough-vol API shape should carry the source SVI snapshot, calibration version, shock controls, static-check status, and residual or premium layer used.

{

"type": "rough_vol_scenario",

"underlying": "BTC",

"source_surface": "derivasys_svi_snapshot_2026-07-08T07:59:28Z",

"backbone": "term_structured_rough_bergomi",

"short_layer": "smooth_total_variance_premium",

"shock_controls": {

"forward_variance": "+1.0 sigma",

"wing_intensity": "+20%",

"skew_correlation_tilt": "downside",

"short_premium": "+35%"

},

"diagnostics": {

"calendar_total_variance_violations": 0,

"butterfly_proxy_violations": 0,

"call_monotonicity_violations": 0

}

}Reading path

Place rough volatility inside the surface, smile, and scenario workflow.

Rough volatility is not a replacement for SVI, quote cleaning, or surface diagnostics. It sits above the accepted market surface as a dynamic scenario layer.

FAQ

Common rough volatility questions.

What is rough volatility?

Rough volatility is a class of volatility models where volatility moves with rough, irregular time-series behaviour. In options, it is useful because it can generate realistic smile dynamics and strong short-time volatility movement without assuming a smooth volatility path.

What is the rough Bergomi model?

Rough Bergomi is a stochastic volatility model that uses a rough variance process driven by parameters such as the Hurst exponent H, vol-of-vol eta, skew/correlation rho, and an initial forward variance curve xi(t). It is often used as a practical rough-volatility benchmark.

Why does a rough-vol fit fail on very short crypto expiries?

The short end can contain event, jump, flow, and market-microstructure premium that is not implied by extrapolating a medium/long rough-vol backbone. In the Derivasys snapshot, the >=30d fit is good, but the implied <30d fit is far too poor to publish as a pure model.

Why not just widen the calibration bounds?

Widening the bounds only improves the medium/long RMSE by about 0.02 vol points in the current snapshot and pushes parameters to more extreme values. That makes the bound pressure a diagnostic, not a modelling solution.

Why do rough-vol shock surfaces sometimes show lumps?

Lumps appear when raw short-tenor residual grids are shocked directly. The raw overlay is good for an in-sample fit benchmark, but shocks should use a smoother total-variance premium layer or richer event model.

How does Derivasys use rough volatility?

The current Derivasys prototype uses a term-structured rough-vol backbone for medium/long scenarios, a raw short residual overlay as the fit benchmark, and a smooth short-premium layer for parameter-based shocks.

References