The core idea

SSVI turns SVI from expiry slices into a coherent surface.

Raw SVI is usually introduced as a formula for fitting one volatility smile. SSVI, or Surface SVI, keeps the same total-variance mindset but makes the maturity dimension part of the parameterization. The surface is driven by ATM total variance, a skew parameter, and a function that controls how smile steepness changes with expiry.

That makes SSVI useful when the question is not just "can this expiry be fit?" but "does the whole volatility surfacebehave coherently across expiries?" For crypto options, that matters because BTC and ETH term structures can move quickly around events, funding changes, and venue liquidity shifts.

Start with ATM total variance

Build a term structure of theta values, where theta is ATM implied volatility squared times time to expiry.

Choose skew controls

Use rho for signed skew direction and phi(theta) for how steep the smile is at each total-variance level.

Check the whole surface

Review butterfly, calendar, slope, and residual diagnostics before using the surface for risk nodes or API output.

Formula

SSVI formula: total variance with theta, rho, and phi(theta).

A common SSVI form writes total variance as a function of log-moneyness k and ATM total variance θ. The parameter ρ sets the signed skew direction, while φ(θ) controls how strongly the slice bends for that total-variance level.

In practical systems, θ comes from the accepted ATM term structure, not from a single raw quote. That connects SSVI directly to forward volatility checks and calendar diagnostics.

Parameter diagnostics

The SSVI parameters should be reviewed as live surface controls.

SSVI is useful because the parameters are operationally meaningful. Theta tracks the ATM total-variance term structure, rho lines up with signed skew and risk reversals, and phi(theta) controls how smile steepness decays as maturity changes. Those values should be plotted and alerted like any other production surface signal.

theta

ATM total variance anchors the expiry level. It should line up with the accepted ATM term structure, fixed-tenor rows, and forward-volatility checks.

rho

Rho controls signed skew direction. In crypto, it should be reviewed beside 25-delta risk reversals and the venue marks driving the wing.

phi(theta)

Phi controls how quickly smile steepness changes with total variance. Large or jagged phi values are usually a warning about interpolation or weak wing data.

theta phi product

The product links term structure and wing slope. Monitoring it makes SSVI useful as a surface-quality diagnostic, not just a formula.

Parameter guards

SSVI parameter bounds and movement checks should be enforced before publication.

SSVI has fewer controls than independent raw SVI slices, so each control has more influence. A production implementation should track parameter bounds, previous accepted values, and the risk nodes affected by each parameter move.

Theta curve

Theta should be positive, ordered by maturity, and explainable by the accepted ATM term structure rather than a single stale quote.

Rho range

Rho must remain inside practical skew bounds. Values near -1 or 1 imply extreme one-sided wings and should trigger review.

Phi smoothness

Phi(theta) should not jump between neighboring maturities unless the live smile evidence and residuals justify the move.

Theta-phi product

The theta times phi product controls wing slope and should be monitored beside risk reversals, flies, and extrapolated deltas.

SVI vs SSVI

Raw SVI is a slice fit; SSVI is a surface shape.

The two are complementary. A live dashboard can fit raw SVI on each expiry because it is flexible and direct. SSVI is useful when the system needs a lower-dimensional surface view, extrapolation discipline, or clearer static-arbitrage reasoning across maturities.

Raw SVI

Fits each expiry with five slice parameters: a, b, rho, m, and sigma. It is flexible and practical for live per-expiry calibration.

SSVI

Uses ATM total variance and a lower-dimensional surface shape, so expiry slices are tied together through the term structure.

Production workflow

A desk may still fit raw SVI slices first, then use SSVI-style checks to reason about calendar consistency and extrapolation.

Calibration workflow

A production SSVI fit starts with accepted raw slices, not raw exchange quotes.

In a live crypto options stack, SSVI should sit after quote hygiene, forward construction, and raw SVI slice review. That keeps the surface-level fit tied to the same provenance as the dashboard: accepted marks, rejected nodes, residuals, and term-structure diagnostics.

Fit accepted slices first

Start from cleaned option marks and raw SVI slices so stale quotes, crossed markets, and bad wings are already rejected.

Extract surface anchors

Use accepted ATM total variance, observed skew, and smile curvature as anchors before solving for a surface-level shape.

Constrain the surface fit

Keep parameter moves bounded and inspect calendar, butterfly, wing-slope, and residual diagnostics after every accepted update.

Publish with provenance

Expose source expiries, rejected nodes, fit residuals, and dashboard links so API consumers can tell whether the surface is usable.

accepted quotes -> SVI slices -> theta/rho/phi controls -> SSVI surface -> residual and arbitrage gatesCalibration objective

The SSVI calibration objective should balance residual fit with surface stability.

A useful SSVI optimizer is not only trying to lower residuals. It has to preserve the accepted raw slices, keep the theta curve coherent, avoid wing-slope instability, and produce a surface that can be used by risk reversals, flies, variance, local-vol, and dashboard/API consumers.

Weighted residuals

Fit the surface to accepted total-variance slices with weights for quote freshness, liquidity, moneyness, and expiry importance.

Term-structure penalty

Penalize theta, rho, and phi moves that create unstable forward-volatility buckets or unexplained calendar shape changes.

Slice agreement

Keep the SSVI surface close enough to accepted raw SVI slices that users can trace risk nodes back to live marks.

Reject taxonomy

Store whether a failed update came from quote quality, theta curve shape, wing slope, residuals, or calendar consistency.

objective = weighted_total_variance_residuals + theta_curve_penalty + wing_slope_penalty + calendar_consistency_penalty + distance_from_previous_accepted_surface

Production checks

SSVI still needs live calibration, residual, and arbitrage checks.

The Gatheral-Jacquier SSVI construction gives a clean way to reason about static arbitrage, but it does not remove the need for market-data hygiene. A production surface still needs stale quote filters, venue provenance, residual panels, and neighboring-expiry checks.

ATM variance is non-decreasing

The theta term structure should not imply less total variance for a later expiry at the same surface state.

Skew does not explode

The product theta times phi(theta) controls wing slope. Large values can make an otherwise smooth-looking surface unusable.

Calendar buckets remain coherent

Neighboring SSVI slices should imply plausible forward volatility between expiries, not negative or unstable forward variance.

Residuals still matter

A parametric surface can be arbitrage-aware and still miss live venue marks, so residual and quote-through-fit panels stay important.

No-arbitrage diagnostics

SSVI makes arbitrage review easier, but the implementation still has to prove each accepted state.

The practical value of SSVI is that calendar, butterfly, and wing-slope issues can be monitored as surface-level signals. In Derivasys terms, those checks belong beside forward volatility, flies, quote-through-fit residuals, and venue-provenance panels.

Calendar monotonicity

Total variance should increase with maturity. A negative forward-variance bucket means the surface is not ready for downstream risk or local-volatility work.

Butterfly behavior

Each smile slice should imply plausible density across strikes, including wings that are mostly extrapolated rather than actively quoted.

Wing-slope controls

The left and right wing slopes should remain inside practical bounds and should not jump because one expiry has thin liquidity.

Residual review

No-arbitrage shape is not enough. The fitted SSVI surface still has to explain live quotes closely enough for the dashboard or API use case.

API output

An SSVI API should expose the surface controls and diagnostics, not only fitted values.

Downstream systems need to know whether a surface was accepted, reused, stale, or rejected. The API state should therefore carry the SSVI controls, source slices, residuals, no-arbitrage diagnostics, and the published risk nodes derived from the surface.

underlying, currency, expiry set, accepted SVI slice ids, ATM theta curve, and fit timestamp.

rho, phi(theta), theta-phi product, parameter bounds, optimizer status, and previous accepted parameter distance.

weighted residuals, calendar status, butterfly status, wing-slope status, rejected nodes, and stale-surface flag.

ATM rows, risk reversals, flies, fixed-tenor rows, forward-volatility buckets, and source-surface version.

This is the same monitoring problem covered in the production monitoring article: a fit value is not enough unless the dashboard and API also show freshness, provenance, and reject reasons.

Failure modes

SSVI failures usually come from weak inputs, over-smoothing, or hidden fallback state.

Because SSVI couples expiries together, one bad surface input can affect multiple downstream risk nodes. Failed states should be labelled explicitly rather than smoothed into a plausible chart.

Smooth but unsupported surface

A low-dimensional SSVI shape can look coherent while still missing live venue marks, especially in sparse wings.

Theta curve contamination

A stale ATM quote can bend the whole term structure and create bad forward-volatility buckets.

Over-tight surface coupling

Forcing all expiries into one smooth shape can hide a real event premium or a venue-specific quote problem.

Unlabelled fallback state

If a live SSVI update is rejected, the dashboard and API should say whether the previous surface was reused.

Dashboard workflow

Derivasys treats SSVI as part of the surface-quality workflow.

Derivasys exposes the operational objects around a fit: fitted smiles, risk reversals, flies, fixed-tenor rows, quote-through-fit panels, and fit diagnostics. SSVI belongs in that workflow as a surface-level check on whether expiry slices and term structure are telling a coherent story.

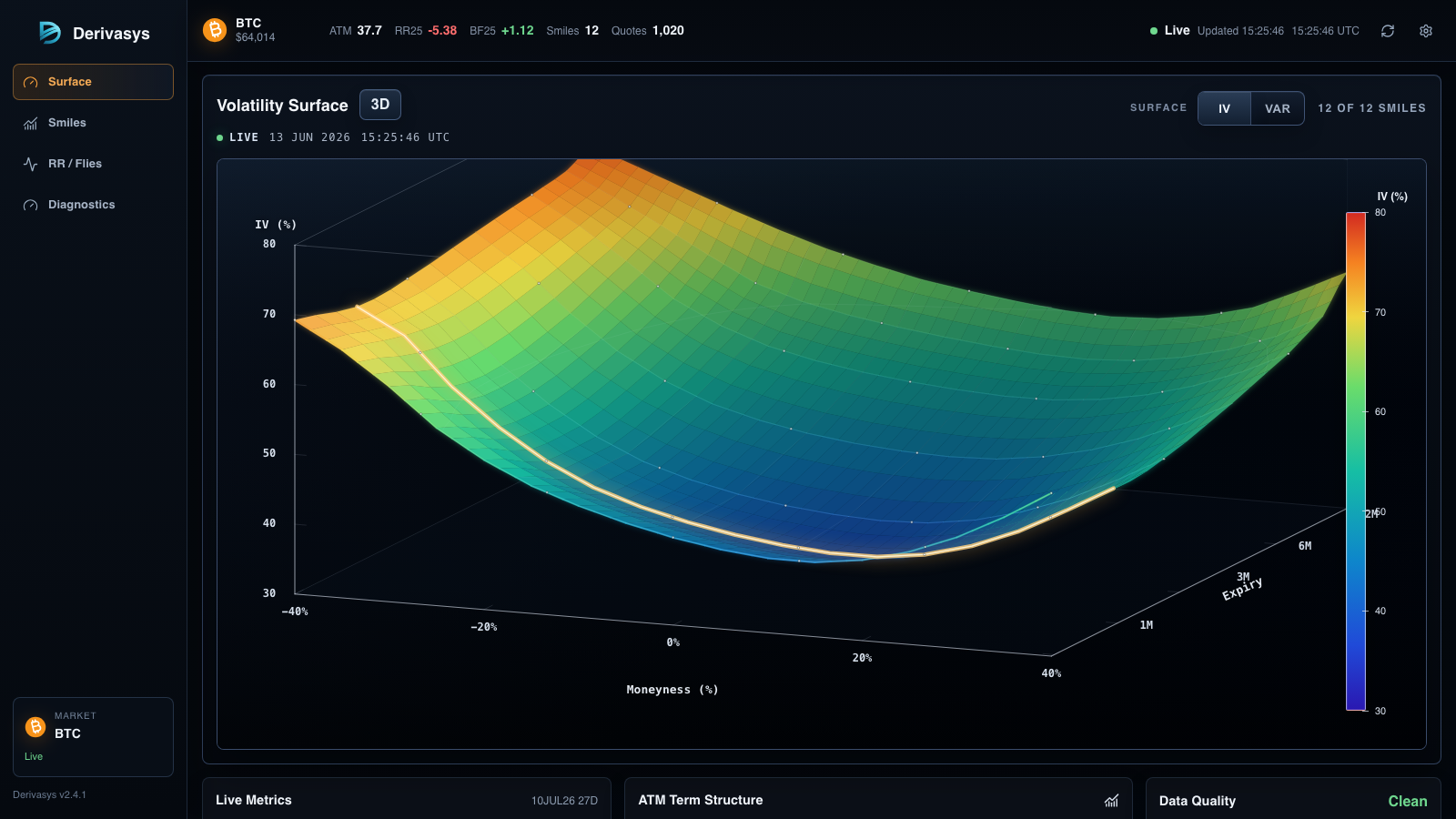

Dashboard screenshots

SSVI diagnostics should stay close to the live fit and residual views.

A surface-level parameterization is only useful if the accepted surface can be traced back to observable market data. These Derivasys views show the fitted surface state and through-fit diagnostics that should accompany any SSVI calibration output.

Reading path

Move through the surface cluster.

Start with the raw SVI formula and per-expiry calibration workflow.

Read nextPlace SSVI inside the full strike and maturity surface.

Read nextUse total variance across expiries to inspect forward buckets.

Read nextConnect the rho/skew view to 25-delta call-minus-put volatility.

Read nextUse flies to read curvature and wing richness around the SSVI smile.

Read nextSee why coherent total variance matters for variance-risk payoffs.

Read nextCompare surface fitting with model dynamics from the Dupire formula.

Read nextMonitor fitted smiles, term structure, and surface diagnostics.

Read nextFAQ

Common questions about SSVI.

What is SSVI?

SSVI means Surface SVI. It is a volatility surface parameterization that extends SVI from independent expiry slices into a surface shape driven by ATM total variance, skew, and a function controlling smile steepness.

How is SSVI different from SVI?

Raw SVI fits one expiry at a time with five parameters. SSVI ties expiries together through the ATM total variance term structure and a surface-level skew function.

Why does SSVI use total variance?

Total variance is the natural object for comparing expiries. Using theta as ATM total variance makes calendar checks, forward-volatility checks, and extrapolation more explicit.

Does SSVI guarantee no arbitrage?

SSVI was designed to make static-arbitrage constraints easier to reason about, but implementation still requires checking the chosen theta curve, skew function, parameter bounds, and live calibration residuals.

How do you calibrate SSVI in production?

A production workflow usually starts from cleaned option marks and accepted SVI slices, then fits the surface-level theta, rho, and phi behavior under residual, calendar, butterfly, and wing-slope checks.

What does phi(theta) control in SSVI?

Phi(theta) controls how smile steepness changes with ATM total variance. It is one of the main diagnostics for whether skew decays smoothly across the term structure.

What is the SSVI calibration objective?

A practical SSVI calibration objective minimizes weighted total-variance residuals across accepted expiry slices while penalizing unstable theta, rho, phi, calendar, and wing-slope behavior.

What should an SSVI API expose?

An SSVI API should expose the accepted SVI slice ids, theta curve, rho, phi(theta), parameter bounds, residuals, arbitrage diagnostics, stale-surface status, and published risk nodes.

When should an SSVI update be rejected?

An SSVI update should be rejected when quote provenance is weak, residuals are too large, theta is not monotonic, wing slopes exceed bounds, or calendar and butterfly diagnostics fail.

References

Primary source and related Derivasys guides.

This guide is written for the Derivasys volatility-surface workflow and links back to the SVI literature and production diagnostics used elsewhere in the cluster.

- Gatheral and Jacquier, Arbitrage-free SVI volatility surfaces

- Derivasys SVI guide

- Derivasys volatility surface guide

- Derivasys forward volatility guide

- Derivasys risk reversals guide

- Derivasys flies guide

- Derivasys variance swaps guide

- Derivasys local volatility guide

- Derivasys arbitrage constraints

- Derivasys production monitoring article

- Derivasys order-book construction article

- Derivasys technical articles